Interest Rates to Remain Stable, Inflation Projection Revised Upward in 2024

In a notable development, the Reserve Bank of India (RBI) has opted to refrain from raising the repo rate during its recent session, thereby ensuring the preservation of the prevailing interest rate of 6.50%. This decision marks the third consecutive instance in which the RBI has elected to maintain rates unaltered, underscoring a judicious and measured approach to monetary policy. The announcement was made by RBI Governor Shaktikanta Das following the conclusion of the monetary policy meeting.

In a strategic recalibration, the Reserve Bank of India (RBI) has revised its inflation projection for the fiscal year 2023-24 (FY23-24) to 5.4%, representing an upward adjustment from the earlier forecast of 5.1%. Simultaneously, the RBI has maintained a steadfast stance on the real Gross Domestic Product (GDP) growth estimate for the same fiscal year, with expectations remaining constant at 6.5%. The central bank’s nuanced assessment provides insights into the anticipated trajectory of economic performance in the coming quarters.

Inflation Outlook:

The revised inflation projection underscores the RBI’s meticulous attention to the intricate interplay of economic variables. The upward adjustment to 5.4% for FY23-24 reflects the dynamic nature of inflation dynamics and the evolving economic landscape. This recalibration is emblematic of the central bank’s commitment to monitoring and addressing potential price pressures, while also ensuring the preservation of purchasing power for consumers.

Real GDP Growth Prospects:

While the inflation projection has been revised, the RBI’s steadfastness is evident in its decision to maintain the real GDP growth estimate for FY23-24 at 6.5%. This reflects a strategic affirmation of the underlying economic resilience and growth potential. The consistent outlook for real GDP underscores the RBI’s confidence in the country’s economic recovery trajectory, underpinned by various sectors’ contributions.

Quarterly GDP Anticipation:

Further granularity is offered through the RBI’s delineation of quarterly GDP growth expectations. The projections indicate a dynamic growth pattern, with the first quarter (Q1) potentially witnessing an impressive 8% expansion. Subsequent quarters display a moderated yet robust growth trajectory, with projections of 6.5% in Q2, 6% in Q3, and 5.7% in Q4. This progressive pattern reflects a comprehensive understanding of seasonal economic dynamics and sectoral contributions to the overall GDP.

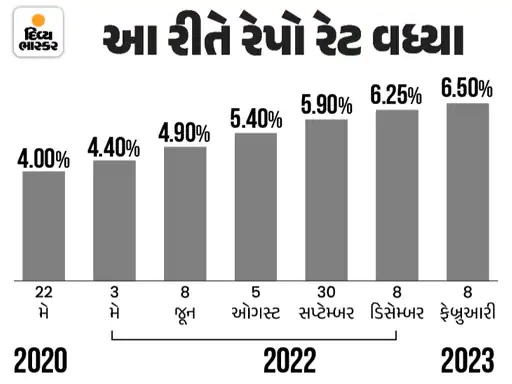

Repo Rate Adjusted Upward by Cumulative 2.50% Through Six Incremental Raises in the Previous Fiscal Year

The realm of monetary policy witnessed a series of noteworthy adjustments in the past fiscal year (FY), with the repo rate experiencing a cumulative upward shift of 2.50% through six consecutive increments. These deliberated adjustments were executed within the context of the Reserve Bank of India’s (RBI) strategic efforts to steer economic dynamics. With the monetary policy meetings occurring bi-monthly, the timeline and magnitude of these adjustments provide insights into the central bank’s response to prevailing economic conditions.

In the backdrop of dynamic economic dynamics, the Reserve Bank of India (RBI) embarked on a strategic path during the fiscal year, juxtaposing steady monetary policy with a decisive emergency response. The narrative unfolds with the RBI’s decision to uphold the repo rate at 4% during its initial policy meeting in April. However, a pivotal juncture materialized in the form of an unprecedented emergency meeting convened on May 2 and 3. This extraordinary gathering precipitated a significant elevation of the repo rate from 4% to 4.40%, mirroring the central bank’s resolute approach to navigating prevailing economic conditions.

In the realm of monetary policy, the repo rate has undergone a series of strategic adjustments, delineating the Reserve Bank of India’s (RBI) measured response to evolving economic dynamics. The following chronicle encapsulates the notable transitions in the repo rate, offering insights into the central bank’s strategic trajectory:

May 22, 2020 – A Pivotal Shift:

A significant juncture in monetary policy materialized on May 22, 2020, marking a substantial change in the repo rate. The rate was elevated, setting the stage for a recalibration of the financial landscape.

June 6-8, 2020 – Incremental Adjustment:

The subsequent policy meeting, convened on June 6-8, 2020, witnessed a further increment in the repo rate by 0.50%. This deliberate step elevated the rate from its prior position of 4.40% to a new threshold of 4.90%.

August 2020 – A Continued Trajectory:

The onward journey of monetary policy led to another noteworthy adjustment in August 2020. During this interval, the repo rate experienced a subsequent increase by 0.50%, bringing it to 5.40%. This strategic move underscored the RBI’s commitment to fine-tuning economic conditions.

September – A Gradual Uptick:

In September, a significant shift manifested in the interest rate framework. The rate experienced an upward trajectory, culminating in an adjustment to 5.90%. This move marked a calibrated step in addressing prevailing economic dynamics.

December – Steady Momentum Continues:

The subsequent phase witnessed the continuation of this upward momentum. By December, the interest rate underwent another increment, ascending to 6.25%. This progression exemplified the RBI’s commitment to fostering stability while considering the evolving economic landscape.

February – Culmination of Fiscal Year 2022-23:

The final monetary policy meeting for the fiscal year 2022-23 was convened in February. During this pivotal gathering, the RBI elected to further elevate interest rates, effectuating a calculated hike from 6.25% to 6.50%. This strategic maneuver underscored the central bank’s comprehensive assessment of economic nuances as the fiscal year reached its culmination.

The Repo Rate as a Tool for Inflation and Economic Management

The Reserve Bank of India (RBI) wields the repo rate as a potent instrument in its arsenal, strategically adjusting it to address distinct economic scenarios. These adjustments play a pivotal role in steering inflation, fostering economic growth, and maintaining financial stability. The rationale behind the RBI’s decisions to increase or decrease the repo rate can be comprehended through the following dynamics:

Controlling Inflation:

High inflation, characterized by an increase in general price levels, can have detrimental effects on an economy. In such circumstances, the RBI resorts to raising the repo rate. By doing so, the central bank aims to reduce the infusion of money into the economy. The heightened repo rate encourages banks to borrow less from the RBI, making these funds relatively expensive. As a result, banks tend to increase interest rates on loans to consumers. This increment in borrowing costs curbs spending and investment, thus decreasing the overall demand for goods and services. Consequently, a reduction in demand helps mitigate inflationary pressures, contributing to price stability.

Stimulating Economic Growth:

During periods of economic downturn or sluggish growth, the RBI deploys a contrasting strategy by lowering the repo rate. This maneuver enhances the availability of cheaper funds for banks, rendering loans more affordable for both financial institutions and consumers. The ensuing reduction in borrowing costs promotes increased borrowing and spending, which, in turn, stimulates economic activity. For instance, amidst the COVID-19 pandemic-induced economic slowdown, the RBI responded by lowering interest rates to encourage borrowing and investment, thereby bolstering the economy’s revival.

The Impact of Reverse Repo Rate Adjustments on the Economy

The reverse repo rate, a significant tool in the Reserve Bank of India’s (RBI) monetary policy toolkit, plays a pivotal role in managing liquidity, influencing borrowing and lending behavior, and ultimately shaping economic conditions. The repercussions of adjustments to the reverse repo rate can be comprehended through the following dynamics:

Liquidity Management:

The reverse repo rate influences the flow of liquidity in the financial system. When the RBI increases the reverse repo rate, it becomes more attractive for banks to park excess funds with the central bank, as they earn higher interest on these holdings. This leads to a reduction in the available funds in the market, thereby tightening liquidity conditions. Conversely, a decrease in the reverse repo rate encourages banks to lend more to the RBI, resulting in increased liquidity in the market.

Inflation Control:

Similar to the repo rate, the reverse repo rate is a tool used by the RBI to manage inflation. When inflation is on the rise, the RBI may increase the reverse repo rate to incentivize banks to park more funds with the central bank. This action reduces the funds available for lending, making borrowing more expensive and curbing spending. As a result, the increase in the reverse repo rate contributes to cooling down demand and mitigating inflationary pressures.

Banks’ Lending Behavior:

Adjustments to the reverse repo rate impact the profitability of banks. When the rate is higher, banks have an incentive to lend less and park more funds with the RBI, which provides a risk-free return. Conversely, a lower reverse repo rate encourages banks to lend more to customers and businesses to earn higher returns. Thus, changes in the reverse repo rate influence the lending decisions of banks, affecting credit availability and economic activity.

Interest Rate Transmission:

The reverse repo rate also has implications for interest rate transmission. Changes in the reverse repo rate can indirectly influence other interest rates in the economy, including deposit rates and lending rates. Banks may adjust their deposit and lending rates based on movements in the reverse repo rate, impacting borrowing and investment decisions of consumers and businesses.